Let’s be honest, losing your job is a gut punch. Beyond the immediate financial stress, there’s that gnawing anxiety about healthcare. “What about my insurance?” “How will I afford a doctor if I need one?” These aren’t just questions; they’re genuine fears that can paralyze you. But here’s the thing: you are not alone, and more importantly, you have options. Finding cheap health insurance for unemployed USA residents isn’t a pipe dream; it’s a reality if you know where to look and, more crucially, how to navigate the system.

I’ve seen countless individuals in this exact situation, feeling overwhelmed and hopeless. My goal here isn’t just to list programs; it’s to walk you through the practical steps, the often-missed details, and the genuine pathways to securing vital health coverage without breaking the bank. Think of me as your personal guide through the sometimes-confusing maze of American healthcare, especially when you’re facing unemployment. Let’s tackle this together, because your health, even during tough times, is non-negotiable.

The Immediate Aftermath | Don’t Panic, Understand Your Options

The moment you’re notified of job loss, your mind probably races. One of the first things that comes up is often COBRA. And yes, COBRA allows you to continue your employer-sponsored health plan. But let me tell you, for most people, COBRA is prohibitively expensive. We’re talking about paying the full premium, plus an administrative fee, which can easily run into hundreds, if not thousands, of dollars a month. It’s a temporary bridge, sure, but rarely a long-term solution for someone looking for truly cheap health insurance for unemployed USA .

So, if COBRA isn’t the silver bullet, what is? The answer, for many, lies primarily in the Health Insurance Marketplace, established by the Affordable Care Act (ACA). This is where the magic of subsidies and special enrollment periods comes into play, making health insurance significantly more affordable than you might imagine. It’s a game-changer for those who find themselves suddenly without employer-sponsored coverage.

Decoding the Affordable Care Act (ACA): Your Lifeline to Affordable Coverage

The Affordable Care Act, often still referred to as Obamacare, is perhaps your most powerful ally in this situation. It created state and federal marketplaces where individuals can shop for health plans. But the true genius of the ACA for the unemployed lies in two key features: premium tax credits (subsidies) and Special Enrollment Periods (SEPs).

Here’s why the “why” of it matters: Losing your job and, consequently, your health coverage, isn’t just a bad day; it’s considered a “qualifying life event.” This triggers a special enrollment period , typically lasting 60 days from the date you lost your coverage. This means you don’t have to wait for the annual open enrollment period to sign up for a new plan. This is crucial because it allows you to get coverage quickly, minimizing any gaps in your healthcare. Trustworthiness here is key: this isn’t a loophole; it’s a built-in protection designed precisely for situations like yours.

When you apply through the health insurance marketplace , your eligibility for financial assistance ( subsidies ) is determined by your estimated income for the year. And here’s where it gets interesting for the unemployed: your income will likely be much lower than it was when you were working. This lower income often qualifies you for significant premium tax credits, which can drastically reduce your monthly premium, making health insurance incredibly affordable, sometimes even free, depending on your circumstances. These subsidies are paid directly to your insurance company, lowering your out-of-pocket costs from day one.

Navigating the Health Insurance Marketplace: A Step-by-Step Walkthrough

Alright, so you know the ACA is your friend. Now, how do you actually use it? It’s simpler than you might think, but attention to detail is crucial.

- Gather Your Information: Before you even log on, have your estimated household income for the current year (post-job loss), Social Security numbers for everyone in your household, and information about your previous health coverage ready. This streamlines the process.

- Visit Healthcare.gov: This is the official federal marketplace. If your state runs its own marketplace (e.g., Covered California, NY State of Health), Healthcare.gov will redirect you.

- Create an Account and Apply: You’ll fill out an application detailing your household, income, and any other relevant information. Be honest and accurate! This is where your eligibility for subsidies and other financial assistance is determined.

- Report Your Job Loss: When asked about qualifying life events, make sure to indicate that you lost your job and your health coverage. This activates your special enrollment period.

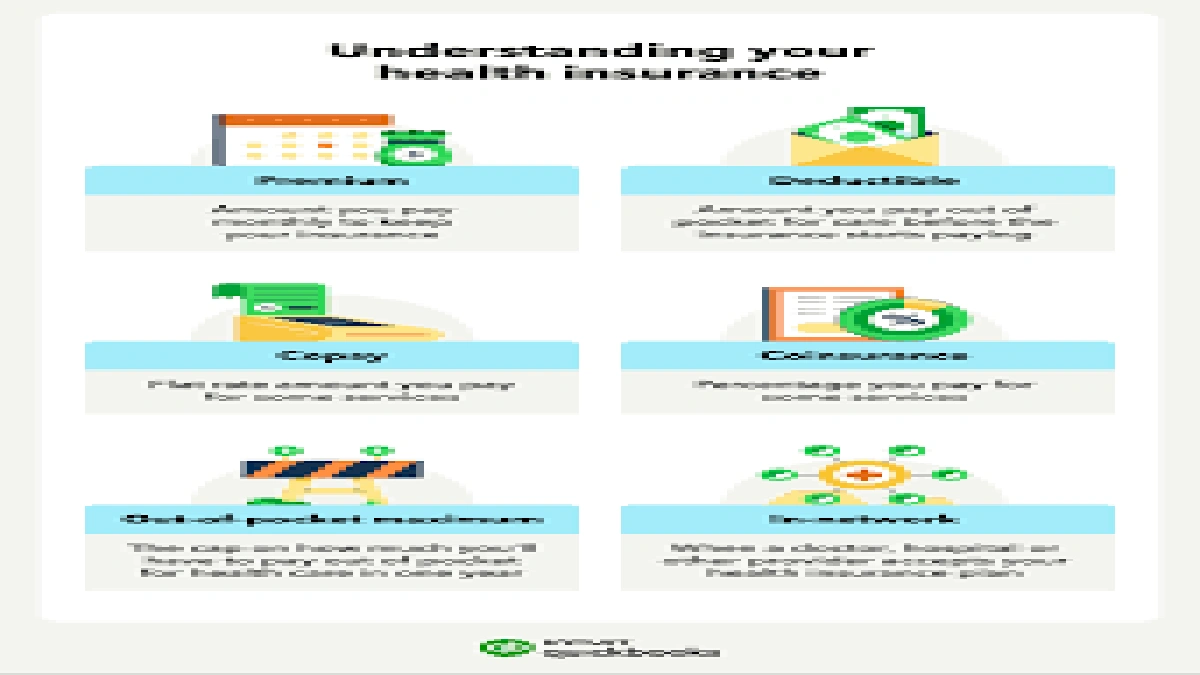

- Compare Plans: Once your eligibility is confirmed, you’ll see a range of plans categorized by metal tiers: Bronze, Silver, Gold, and Platinum. Bronze plans typically have the lowest monthly premiums but higher deductibles and out-of-pocket costs. Silver plans offer a good balance and, for those with lower incomes, may come with additional “cost-sharing reductions” that lower your deductibles, co-pays, and out-of-pocket maximums. This is a vital point for truly cheap health insurance for unemployed USA residents.

- Enroll: Choose the plan that best fits your needs and budget. Remember, the cheapest premium isn’t always the cheapest overall if it means high deductibles you can’t meet. Consider your expected healthcare needs.

The beauty of the marketplace is transparency. You can compare plans side-by-side, seeing what you’ll pay in premiums, deductibles, and out-of-pocket maximums. And don’t forget, if you qualified for subsidies, those are already factored into the prices you see, making the comparison even easier.

Exploring Medicaid | A Crucial Safety Net for Low-Income Individuals

For many facing unemployment, especially those with very low or no income, Medicaid can be an absolute lifesaver. This is a joint federal and state program that provides free or low-cost health coverage to millions of Americans. While the ACA expanded Medicaid eligibility in many states, some states have not yet adopted the expansion.

Here’s the breakdown: If you live in a state that expanded Medicaid, eligibility is primarily based on income relative to the Federal Poverty Level (FPL). You might qualify if your income is below a certain percentage of the FPL (often 138%). If your state hasn’t expanded Medicaid, the eligibility rules can be stricter, often requiring you to meet specific categories like being pregnant, a parent, a child, or having a disability, in addition to low income.

How to check? When you apply through Healthcare.gov, your application will automatically be assessed for Medicaid eligibility. If you qualify, your information will be securely transferred to your state’s Medicaid agency. Alternatively, you can apply directly through your state’s Medicaid website or by visitingMedicaid.govfor general information and links to state programs. This is often the most comprehensive and truly low-cost health plans available for those who meet the criteria.

Beyond the Basics: Other Considerations and Low-Cost Health Plans

While the ACA Marketplace and Medicaid are your primary avenues, it’s worth understanding other options, though they often come with caveats.

Short-Term Health Insurance

These plans are exactly what they sound like: temporary coverage for a limited period (often less than a year, though some can be renewed). They typically have lower premiums than ACA plans but offer fewer benefits, don’t cover pre-existing conditions, and aren’t required to meet the ACA’s essential health benefits. They can be a stop-gap measure if you missed your special enrollment period or are waiting for new employer coverage, but they are not a substitute for comprehensive coverage, especially if you have ongoing health needs. It’s a bit like buying a minimalhome insurance for natural disasters USA– it covers the big, sudden stuff, but not the day-to-day wear and tear or minor issues.

Community Health Centers and Free Clinics

If you find yourself uninsured, or with a plan that has a very high deductible, remember that community health centers and free clinics offer vital services, often on a sliding scale based on your income. They can provide primary care, preventive services, and even some specialty care at significantly reduced costs. They’re an excellent resource for managing basic health needs while you secure more comprehensive coverage.

COBRA Alternatives

As mentioned, COBRA is pricey. The ACA marketplace is generally the best alternative. However, if you’re looking for something very specific and very short-term, some private insurers offer plans that bridge gaps. Always compare these rigorously against marketplace plans, especially after accounting for potential subsidies. The marketplace almost always offers better value and protection for those seeking genuinely cheap health insurance for unemployed USA citizens.

Think of finding the right health insurance during unemployment much like an entrepreneur seekingcheap business insurance for startups. You need to be resourceful, understand the unique risks, and leverage every available program to protect your most valuable asset – in this case, your health. It’s about smart, strategic planning, not just picking the lowest sticker price.

Navigating unemployment is undoubtedly one of life’s tougher challenges. But losing your job doesn’t mean you have to sacrifice your health or go into massive debt for medical care. The system, while complex, has built-in safety nets designed to help you. By understanding the Affordable Care Act , the health insurance marketplace , and Medicaid , you can find genuinely affordable, quality coverage. Don’t let fear or misinformation keep you from seeking the care you deserve. Take action, explore these options, and secure your health during this transition.

Frequently Asked Questions (FAQs)

How do I apply for cheap health insurance for unemployed USA?

The primary way to apply is through the Health Insurance Marketplace at Healthcare.gov. Losing your job qualifies you for a Special Enrollment Period (SEP), allowing you to sign up outside of open enrollment. Your application will also check for Medicaid eligibility.

What is a special enrollment period?

A Special Enrollment Period (SEP) is a designated time outside of the annual Open Enrollment Period when you can sign up for health insurance. Losing your job and employer-sponsored coverage is a common qualifying life event that triggers a 60-day SEP.

Can I get Medicaid if I was just laid off?

Yes, potentially. If your income falls below a certain threshold due to unemployment, you may qualify for Medicaid, especially if you live in a state that expanded its Medicaid program under the ACA. Your application through Healthcare.gov will assess your eligibility.

Are short-term health insurance plans a good option?

Short-term plans can be a temporary solution for very specific situations, like bridging a small gap in coverage. However, they are not comprehensive, often don’t cover pre-existing conditions, and don’t offer the same consumer protections or essential health benefits as ACA-compliant plans. They are generally not recommended as a long-term solution for unemployed individuals.

What if I have no income at all?

If you have no income or very low income, you are highly likely to qualify for significant subsidies through the Health Insurance Marketplace, potentially bringing your monthly premium down to zero. You may also be eligible for Medicaid, which offers free or very low-cost comprehensive coverage.