Alright, let’s be honest. When you hear “professional indemnity insurance UK cost,” your eyes might glaze over a little. It sounds like one of those necessary evils, a bureaucratic hurdle between you and getting on with your actual work. But here’s the thing: understanding your professional indemnity insurance UK cost isn;t just about ticking a box; it’s about protecting your livelihood, your reputation, and your peace of mind. And trust me, navigating the ins and outs doesn’t have to be a headache. I’ve seen countless professionals struggle with this, and my goal today is to cut through the jargon and give you a clear, actionable guide.

Think of it like this: you’re a professional, offering your expertise, advice, or services. What happens if, despite your best intentions, a client alleges you made a mistake, gave negligent advice, or failed to perform a service adequately? That’s where professional indemnity (PI) insurance steps in. It’s not just for doctors or lawyers anymore; consultants, IT professionals, marketing agencies, architects, even freelance writers – if you offer a service that could lead to financial loss for a client, you need to pay attention. We’re going to break down not just what impacts your premiums, but practical strategies forreducing professional indemnity premiumswithout compromising on crucial coverage.

Why Professional Indemnity Insurance Isn’t Just a ‘Nice-to-Have’ in the UK

In the UK, the professional landscape is evolving. Clients are savvier, and the legal framework, while designed to protect everyone, can sometimes feel like a minefield for businesses. Professional indemnity insurance isn’t just a regulatory requirement for some professions (like solicitors or financial advisors); it’s a strategic shield for almost anyone offering a service. I often hear people say, “But I’m careful! I won’t make a mistake.” And that’s commendable! But remember, PI insurance covers not just actual errors, but allegations of errors. Even if you’re entirely blameless, defending yourself against a claim can be incredibly costly in terms of legal fees, time, and reputational damage. This is where your PI policy becomes invaluable, covering legal defence costs, compensation, and damages.

Consider the broader context: the rise of the gig economy and independent contractors means more individuals are directly exposed to these risks. A sole trader, for instance, doesn’t have a large corporate entity to absorb a legal challenge. Their personal assets could be at stake. This is a crucial ‘why’ behind the importance of understanding your professional indemnity insurance UK cost – it’s an investment in your business’s resilience. It also enhances your credibility, as many larger clients will actually insist you have adequateindemnity insurancebefore they even consider working with you.

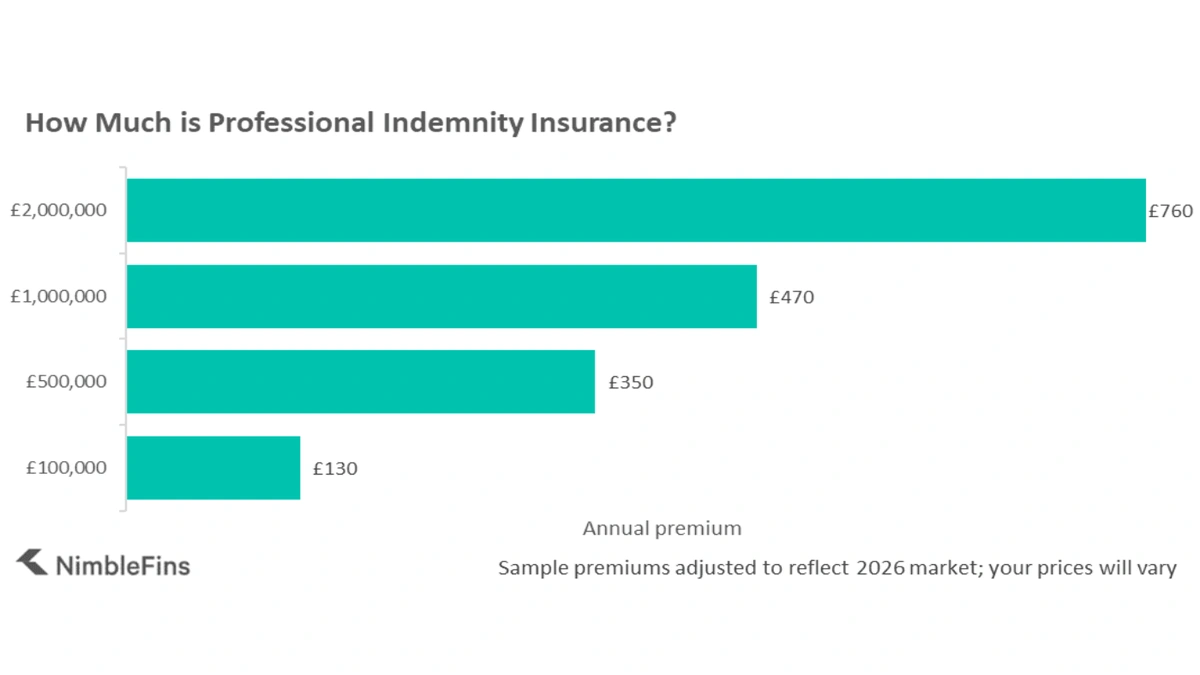

The Great Cost Conundrum | What Really Drives Your PI Premiums?

So, you’ve decided you need it. Now, the big question: how much is professional indemnity insurance going to set you back? There’s no single answer, unfortunately. It’s not like buying a loaf of bread. The cost is highly individualised, a complex calculation based on several key factors. Let me walk you through the primary drivers that influence yourinsurance premium:

- Your Profession & Industry Risk: This is arguably the biggest factor. A management consultant faces different risks than an architect. Professions with higher potential for financial loss or bodily injury (e.g., medical professionals, structural engineers) will naturally have higher premiums. Insurers assess the inherent risk of your specific services.

- Your Turnover & Business Size: Generally, the larger your turnover, the higher your potential liability. More revenue often means more clients, bigger projects, and thus, a greater exposure to risk. Similarly, a larger team might increase the likelihood of an error, even with robust internal controls.

- Coverage Limits & Excess: This is straightforward: higher coverage limits (the maximum amount the insurer will pay out) mean higher premiums. Your excess (the amount you pay towards a claim before the insurer contributes) also plays a role. A higher excess typically leads to a lower premium, but means more out-of-pocket expense if you do claim.

- Claims History: If your business (or you, if you’ve been insured previously) has a history of claims, insurers will view you as a higher risk, pushing up your professional indemnity insurance UK cost.

- Contractual Obligations: Some clients or industry bodies might stipulate a minimum level of PI coverage. This can sometimes push you towards higher limits than you might have otherwise chosen.

- Geographical Reach: While we’re talking about the UK, if your services extend internationally, particularly to places like the US or Canada, your risk exposure (and thus cost) can increase significantly due to different legal systems and higher potential damages.

Understanding these factors affecting PI insurance cost is the first step towards getting sensible PI insurance quotes UK and finding the right policy for you.

Smart Strategies to Reduce Your Professional Indemnity Insurance UK Cost

Now for the good stuff: how can you actively work towards getting the cheapest professional indemnity insurance without leaving yourself exposed? It’s not about cutting corners; it’s about smart risk management and informed choices.

- Shop Around (and Use a Broker!): This is non-negotiable. Don’t just accept the first quote. Different insurers have different appetites for risk and specialise in different sectors. An independent insurance broker can be a huge asset here. They have access to multiple underwriters and can often negotiate better deals than you might find yourself. They also understand the nuances of professional liability insurance UK market.

- Accurate Information is Key: When getting quotes, be meticulously accurate with your business details, turnover projections, and services offered. Understating your risk might get you a cheaper initial quote, but it could invalidate your policy later. Overstating it will just lead to higher premiums.

- Review Your Coverage Limits Annually: Your business evolves. So should your insurance. Is that £1 million coverage still appropriate if your biggest project is now £50,000? Or vice-versa? Don’t pay for more than you need, but certainly don’t under-insure. This risk assessment should be an annual exercise.

- Increase Your Excess: As mentioned, a higher excess can lower your premium. If your business has strong cash flow and you’re comfortable taking on a larger initial hit in the event of a minor claim, this can be an effective way to save.

- Implement Robust Risk Management: Show insurers you’re proactive. This means having clear contracts, detailed record-keeping, robust quality control processes, and formal client complaint procedures. Documenting these can sometimes lead to better rates, as it demonstrates a lower likelihood of claims.

- Consider Packaging Policies: Sometimes, combining your PI insurance with other policies like public liability or employers’ liability can result in a discount compared to buying them separately. This is often called a ‘business package’ and is worth exploring, especially for UK businesses.

Remember, the goal isn’t just the lowest professional indemnity insurance UK cost, but the best value – comprehensive cover at a competitive price for your specific needs. This proactive approach to reducing professional indemnity premiums truly pays off.

Choosing the Right Policy | More Than Just the Price Tag

Let me rephrase that for clarity: don’t let the quest for the lowest professional indemnity insurance UK cost blind you to the quality and breadth of coverage. A cheap policy that doesn’t cover your specific risks is, frankly, useless. When comparing PI insurance quotes UK, look beyond the headline figure:

- Retroactive Cover: Does the policy cover work you did in the past? Many claims arise years after a project is completed. This is crucial for continuity.

- Defence Costs: Are legal defence costs included within or in addition to your main limit of indemnity? This can make a huge difference in how much cover you actually have for a claim.

- Specific Exclusions: Read the small print! Are there any specific activities or types of work that are excluded? For instance, some policies might exclude work undertaken in certain high-risk industries or geographical locations.

- Policy Wording & Clarity: Is the policy wording clear and understandable? If you’re unsure, ask your broker to explain. A good broker will demystify terms like ‘claims-made’ vs. ‘occurrence-based’ policies.

Your business is unique, and your professional negligence insurance cost reflects that. Tailoring your policy to your exact requirements, rather than just picking a generic option, ensures you’re properly protected.

Navigating the Claims Process | A Quick Word of Caution

Even with the best intentions and the most robust risk management, claims can happen. The key is to act swiftly and correctly. The moment you become aware of a potential claim, or even an incident that could lead to a claim, notify your insurer immediately. Don’t wait. Many policies have strict notification clauses, and delaying could jeopardise your coverage. Your insurer will guide you through the process, but your prompt action is vital. This proactive approach not only helps you but also reinforces your trustworthiness with the insurer, potentially influencing future professional indemnity insurance UK cost assessments.

Frequently Asked Questions About Professional Indemnity Insurance UK Cost

How often should I review my professional indemnity insurance?

You should review your policy at least annually upon renewal, but also whenever there’s a significant change in your business, such as taking on larger projects, expanding your services, or increasing your turnover. This ensures your coverage limits remain appropriate.

Can I get professional indemnity insurance for past work?

Yes, this is known as ‘retroactive cover’ or ‘prior acts cover’. Most professional indemnity policies are ‘claims-made’, meaning they cover claims made during the policy period, regardless of when the work was done, as long as you had continuous cover from the time the work was performed. Always check your policy wording carefully.

What happens if I cancel my policy early?

If you cancel your professional indemnity policy early, you might receive a pro-rata refund for the unused portion of your premium, depending on the insurer’s terms. However, be aware that cancelling means you will no longer be covered for new claims arising after the cancellation date, even if they relate to work done previously (unless you purchase ‘run-off’ cover).

Is professional indemnity insurance mandatory for all professions in the UK?

No, it’s not mandatory for all professions. However, it is a regulatory requirement for many, including solicitors, accountants, financial advisors, and architects. Even where not mandatory, it’s highly advisable for any professional offering advice or services that could lead to a client’s financial loss.

How does my business size affect the professional indemnity insurance UK cost?

Generally, larger businesses with higher turnovers and more employees tend to have higher professional indemnity insurance UK cost. This is because increased scale often means greater exposure to potential claims and higher potential damages if a claim is successful. However, larger businesses might also benefit from economies of scale in some aspects of their insurance arrangements.

So, there you have it. The world of professional indemnity insurance UK cost might seem daunting at first, but with a clear understanding of the factors at play and a proactive approach to managing your risk and shopping for policies, you can secure the vital protection you need without breaking the bank. It’s not just an expense; it’s an intelligent investment in your professional future. Now go forth, confident and covered!