Alright, let’s be honest. Nobody wants to think about life insurance payouts. It means someone you care about deeply is no longer here. It’s a tough conversation, a somber reality. But here’s the thing: when that moment inevitably arrives, understanding thelife insurance payout optionsavailable in the USA can make a monumental difference for you and your family’s financial future . It’s not just about receiving money; it’s about making smart, informed decisions during what will undoubtedly be a challenging time. Trust me, I’ve seen countless beneficiaries overwhelmed by the choices, often making hasty decisions they later regret. My goal here? To guide you through it, step-by-step, like a knowledgeable friend over a cup of coffee, so you feel empowered, not lost.

You see, a life insurance policy isn’t just a piece of paper; it’s a promise, a financial safety net. But that net comes with different ways to deploy it. Should you take a single, large sum? Or would a steady stream of income be more beneficial? What about the dreaded tax implications ? These aren’t just theoretical questions; they’re real-world dilemmas that impact everything from daily expenses to long-term investment strategies. So, let’s roll up our sleeves and demystify the process, ensuring you’re equipped to handle whatever comes your way.

Understanding the Basics | What Happens After a Claim?

When a life insurance claim is filed, it kicks off a process that can feel opaque if you’re not prepared. First, the insurance company verifies the claim. This involves checking the policy, confirming the death, and ensuring all documentation is in order. Once approved, that’s when the real decisions begin for the beneficiary . Most policies offer a few core settlement options , and knowing them beforehand is half the battle won.

A common mistake I see people make is assuming there’s only one way to receive the money: a big check. While a lump sum is indeed the most common and often the default, it’s far from the only choice. The insurance company isn’t going to hand-hold you through the nuances of each option; that’s where this guide comes in. Think of it as your personal roadmap to understanding these cruciallife insurance payout options explained USA, helping you navigate the complexities with confidence.

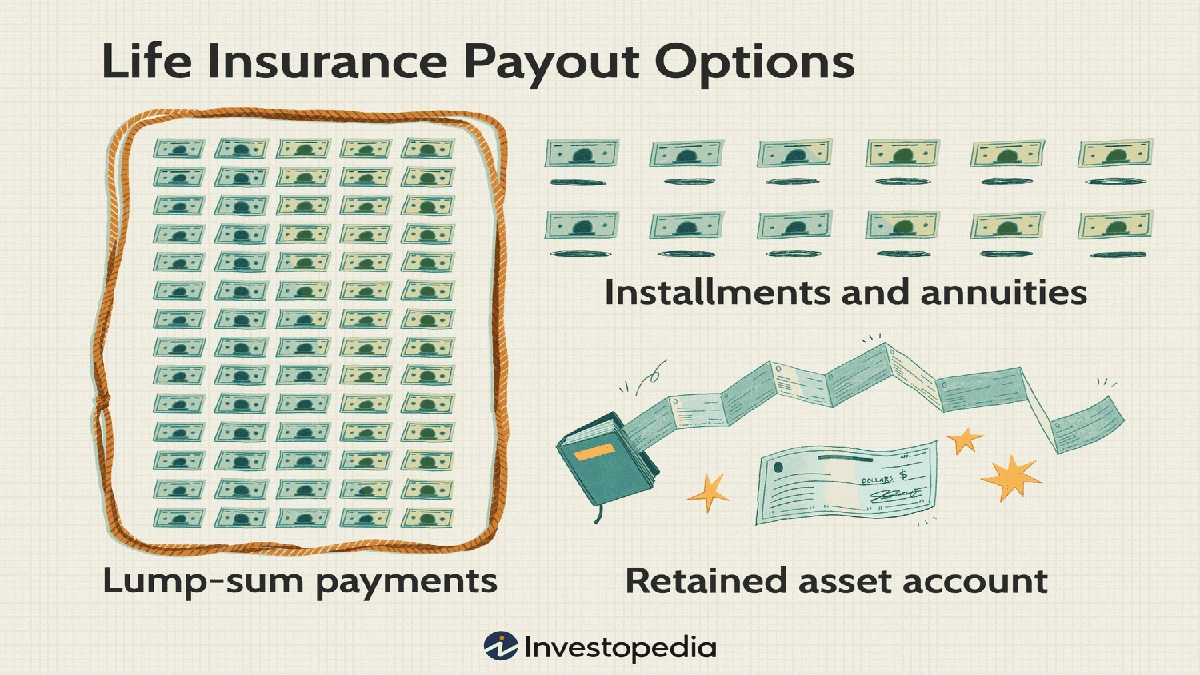

The Big Choices | Lump Sum vs. Annuity vs. Other Settlement Options

This is where the rubber meets the road. Each option has its own set of pros and cons, and what’s right for one person might be entirely wrong for another. It truly depends on your immediate needs, your financial literacy, and your long-term goals. Let’s break down the primary choices:

1. Lump Sum Payment

This is exactly what it sounds like: the entire death benefit paid out in one single payment. It’s the most straightforward and gives the beneficiary immediate access to all the funds. Many people prefer this for its simplicity and the ability to control the money entirely. You can pay off debts, make a large investment, or use it for immediate needs. However, the downside is that managing a large sum of money, especially during a period of grief, can be incredibly daunting. Without proper financial planning, it’s easy to make impulsive decisions or fall victim to scams. It requires discipline and often, professional financial advice.

2. Annuity (Settlement Option)

Instead of a single payment, an annuity provides regular payments over a set period or for the rest of the beneficiary’s life. The insurance company essentially holds onto the death benefit and pays it out with interest. This can be an excellent option for those who aren’t comfortable managing a large sum, or who need a steady income stream to cover living expenses. It provides predictability and peace of mind. The trade-off? You lose immediate access to the full amount, and the overall return might be less than if you had invested a lump sum wisely yourself. There are different types of annuities, like fixed period (payments for a specific number of years) or life annuity (payments for life).

3. Interest Option

With this option, the insurance company holds the death benefit and pays the beneficiary only the interest earned on that money. The principal sum remains with the insurer until a later date when the beneficiary decides to take it as a lump sum or convert it into an annuity. This can be useful for beneficiaries who don’t need the money immediately but want to ensure it’s growing and accessible when they do. It’s a good way to defer a major financial decision until you’re in a clearer headspace.

4. Fixed Period or Fixed Amount Options

These are variations where the beneficiary chooses either to receive payments for a specific number of years (fixed period) or to receive a specific payment amount until the funds are exhausted (fixed amount). They offer a middle ground between the lump sum and a lifetime annuity, providing structure without being entirely locked in forever. Understanding these diverse beneficiary choices life insurance policies offer is paramount for informed decision-making.

Decoding the Fine Print | Tax Implications and Other Considerations

Now, let’s talk about something often overlooked: taxes. Generally, the death benefit of a life insurance payout received by a beneficiary is not subject to federal income tax in the USA . That’s a huge relief, right? However, there are crucial exceptions and nuances you absolutely need to be aware of.

For instance, if you choose an interest option or an annuity, any interest earned on the death benefit after the insured’s death typically is taxable. The IRS treats that interest as income. This is a critical detail that can significantly impact your net payout. It’s why I always emphasize consulting with a tax professional or financial advisor when making these decisions. For comprehensive guidance, you can always refer to official IRS publications, likeIRS Publication 505, which covers tax withholding and estimated tax.

Beyond taxes, consider the impact of inflation. A fixed annuity might seem appealing now, but will that payment be sufficient 10 or 20 years down the line? Also, what about your current financial situation? Do you have high-interest debt that a lump sum could eliminate immediately? Or are you a savvy investor who could potentially generate higher returns by investing a lump sum yourself? These are not easy questions, and there’s no one-size-fits-all answer. It’s about aligning the settlement options life insurance offers with your personal circumstances and future needs. Just as you might compare differentprivate family health insurance UK comparisonoptions for healthcare, comparing life insurance payout options requires a similar level of detailed analysis, even if the context is different.

Making the Right Choice | A Step-by-Step Approach for Beneficiaries

Feeling a bit overwhelmed? That’s perfectly normal. But let’s simplify it. Here’s a practical approach to help you decide on the best life insurance payout option for you:

- Assess Your Immediate Needs: Do you have outstanding debts (mortgage, credit cards, medical bills)? Are there immediate funeral expenses or other urgent costs? A lump sum might be necessary to cover these quickly.

- Evaluate Your Financial Literacy & Comfort Level: Are you comfortable managing a large sum of money, investing it, and dealing with market fluctuations? If not, a structured settlement like an annuity might offer more security and peace of mind.

- Consider Your Long-Term Goals: Are you planning for retirement? Funding a child’s education? Starting a business? Your long-term aspirations will heavily influence whether a steady income stream or a large upfront capital injection is more suitable.

- Factor in Your Age and Health: If you’re younger, a longer-term annuity might seem less appealing than a lump sum you can invest aggressively. If you’re older, a guaranteed income for life could be invaluable.

- Seek Professional Advice: This is perhaps the most crucial step. Consult a qualified financial advisor and a tax professional. They can help you understand the specific implications of each option based on your unique financial situation, including the subtle aspects of tax implications life insurance payout. They can also help you create a comprehensive financial plan that incorporates this new asset.

Remember, this isn’t a race. Most insurance companies will allow you a reasonable amount of time to make this decision. Don’t rush it. Take a deep breath, gather your thoughts, and leverage the expertise of professionals.

Common Questions About Life Insurance Payouts

What is the typical life insurance claim process timeline?

Generally, once all necessary documentation is submitted (death certificate, policy information, claimant statement), a life insurance company in the USA aims to process the claim within 30 to 60 days. However, complex cases, missing documents, or investigations (especially if the policy was very new) can extend this timeline. It’s always best to communicate regularly with the insurer.

Are life insurance payouts taxable?

The death benefit itself is typically not subject to federal income tax. However, any interest earned on the death benefit after the insured’s death (e.g., if the money is held by the insurer in an interest-bearing account or paid out as an annuity with interest) usually is taxable income to the beneficiary . State taxes can vary, so consult a tax professional.

Can I change my payout option after I’ve made a choice?

In most cases, once you’ve formally elected a settlement option and the payments have begun, it’s very difficult, if not impossible, to change it. This is why it’s so vital to make an informed decision upfront. Always clarify this with the insurance company before finalizing your choice.

What if there are multiple beneficiaries?

If there are multiple beneficiaries, the death benefit is typically divided among them according to the percentages specified in the policy. Each beneficiary can then usually choose their preferred life insurance payout options independently for their share, whether it’s a lump sum , annuity, or another option. This can lead to different financial planning for beneficiaries based on individual needs.

What happens if the beneficiary is a minor?

If a minor is named as a beneficiary, the insurance company generally cannot pay the benefits directly to them. Instead, a legal guardian or a court-appointed custodian will typically manage the funds until the minor reaches the age of majority. Often, a trust is set up to handle this situation, ensuring the funds are managed responsibly for the child’s benefit.

Can I use the payout to pay off the deceased’s debts?

Generally, life insurance payout proceeds are paid directly to the named beneficiary and are not considered part of the deceased’s estate for debt purposes. This means creditors usually cannot claim the life insurance money. However, if the estate itself is named as the beneficiary, the funds would then become subject to the estate’s creditors. This is a key distinction in the life insurance claim process .

The Bottom Line | Your Empowered Decision

Navigating the world of life insurance payout options explained USA can feel like a maze, especially during a time of grief. But remember, this isn’t just about money; it’s about securing your future and honoring the legacy of the person who provided this financial protection. By understanding the core choices the immediate control of a lump sum versus the steady security of an annuity , and all the nuanced settlement options in between you’re not just receiving a payout; you’re making an empowered decision that will shape your next chapter. Don’t let the complexity deter you; instead, let it motivate you to seek clarity and make the choice that truly serves your best interests. Your peace of mind is worth every bit of effort.